Being a foreigner doesn't mean you're stuck with bad options

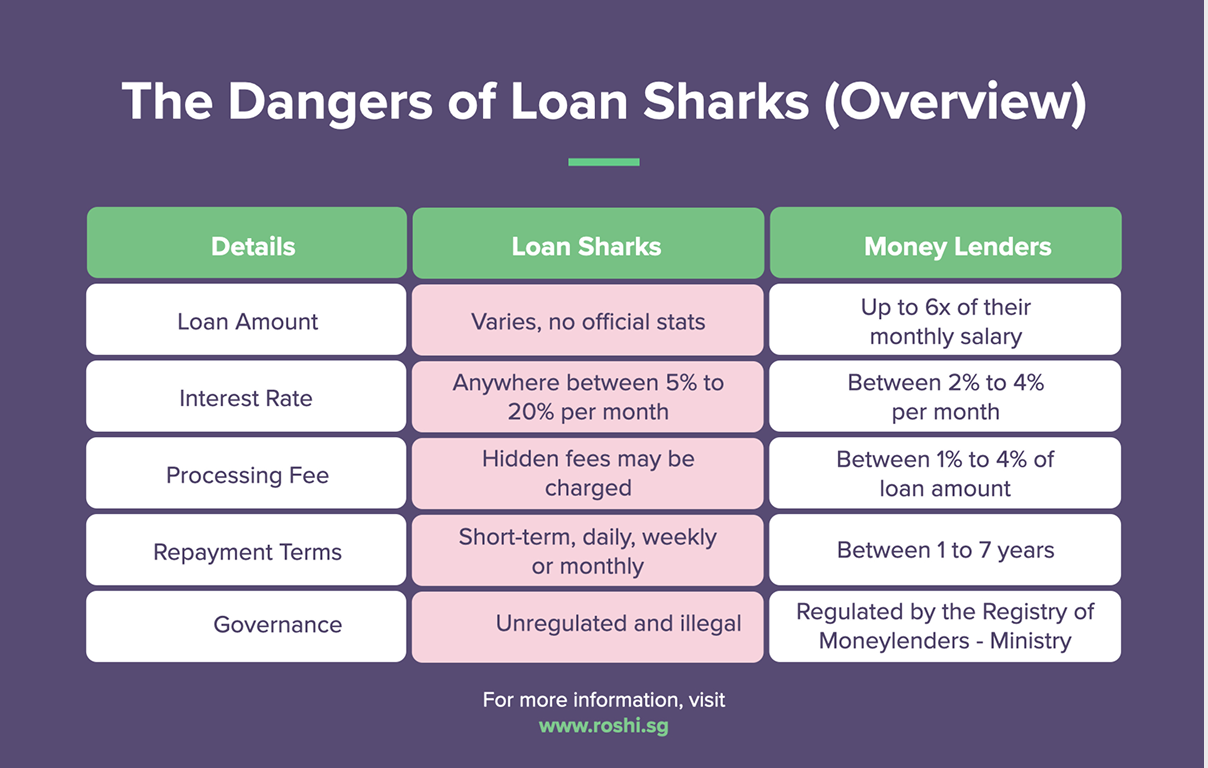

Singapore's moneylending regulations exist to protect borrowers. Interest rates are capped, fees are transparent and every licensed lender must follow the same rules.

The most important thing is to borrow only what you can repay within the agreed repayment timeline. Get your CBS and MLCB reports before applying, have your documents ready and if possible apply early in the month to avoid quota limits. ![]()

![]()

Tips for Foreign Borrowers

How to Improve Your Approval Chances

Your MLCB report shows any outstanding moneylender loans. If you currently have any outstanding loans with other moneylenders, clear those first or make sure your repayment history is clean. Lenders check this before approving your application.

Build local credit history

If you plan to stay in Singapore long-term, get a credit card from a local bank and use it for everyday expenses like groceries and utilities. Pay the full balance monthly. This builds your CBS score over time, which opens the door to bank loans.

Bring a local guarantor

Having a Singaporean or PR act as your guarantor can improve approval chances and may help you secure a lower interest rate. The guarantor must be willing to sign and take on the liability if you default.

Apply early in the month

Licensed moneylenders can only approve 15 foreign borrowers per month. If you apply towards the end of the month, your preferred lender may have already hit their quota.

Only request what you need

Asking for the maximum either $3,000 or $5,000 when you only need $1,500 can reduce your approval chances. Lenders assess whether you can realistically make the repayments so a smaller amount is easier approved.

Ensure your work pass has at least 3 months validity remaining

Lenders need confidence you'll still be employed in Singapore during the repayment period. A pass expiring soon can raise red flags.

Common Mistakes to Avoid

What Foreign Borrowers Get Wrong Most Often

Many foreign loan applications get rejected or end up costing more than they should because of avoidable mistakes. Here are the most common ones we see and how to avoid them.

Interest Rate Trends

In this segment, lending decisions are influenced more by employment pass validity, employer stability and contract duration than by general interest rate movements. As a result, pricing patterns remain largely stable in March with lenders focusing on documentation strength and income continuity rather than broad market shifts. No significant tightening or expansion in credit appetite has been observed.

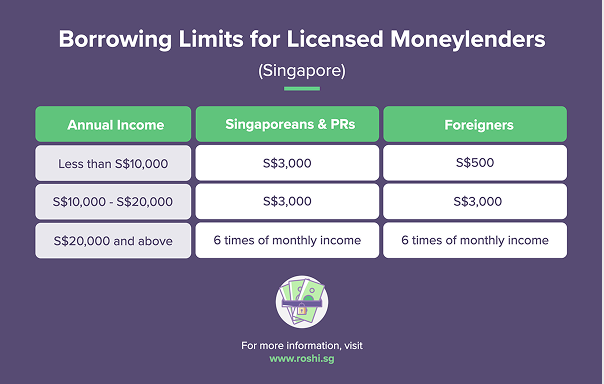

Foreign borrowers may qualify for loans of up to six times their monthly income, subject to valid work passes, proof of employment and salary documentation. In practice, approved amounts are closely aligned with contract length and repayment capacity. Administrative fees remain capped at 10% of the principal and late payment charges generally do not exceed S$60 per month. While initial applications and document submissions are often handled digitally for convenience, Ministry of Law regulations require borrowers to attend a licensed outlet in person to complete identity verification and contractual formalities before funds can be released. Despite this step, many lenders are able to finalise approval and disbursement within the same working day once all documents are verified.

However, documentation standards are more stringent and approval timelines may extend beyond those of licensed moneylenders. Additional scrutiny of employment contracts, minimum annual income requirements and credit standing often limit accessibility for many foreign workers. Consequently, while banks may provide a cost advantage for well-qualified expatriates, they remain less practical for applicants seeking faster processing or short-term financing.

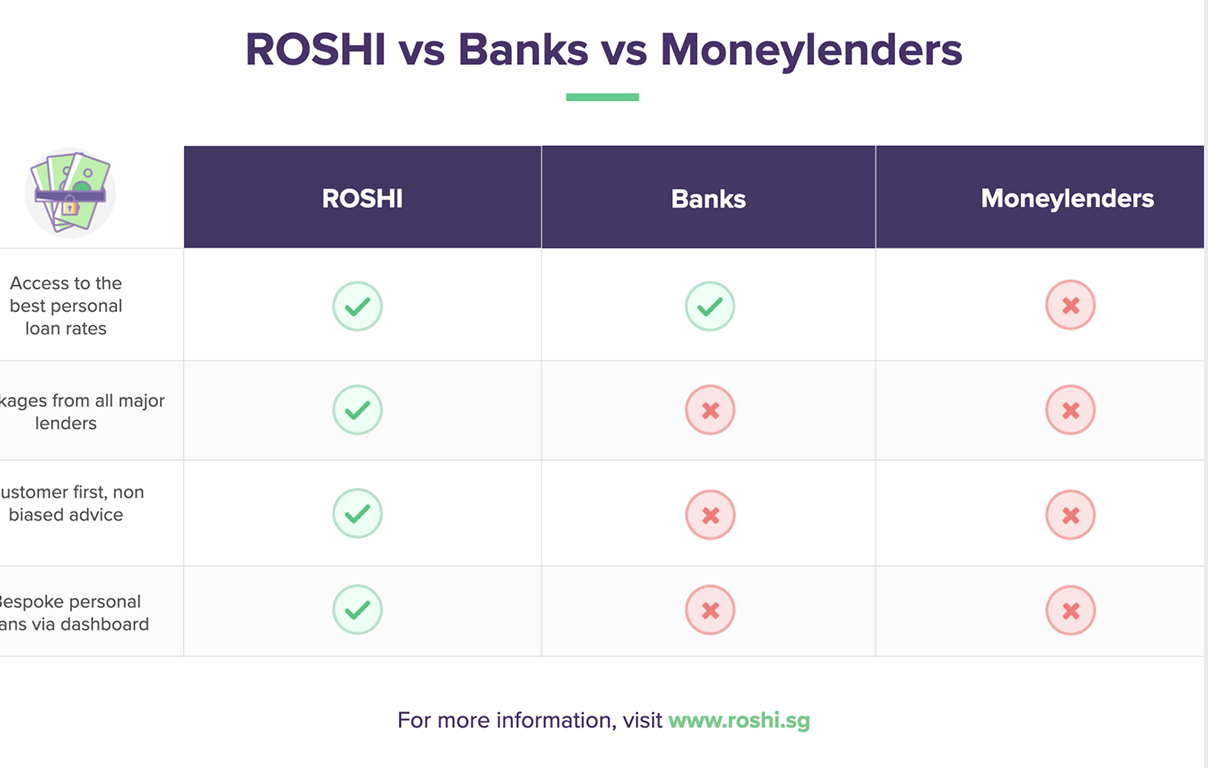

From ROSHI’s perspective, foreigner loans require careful alignment between loan tenure and employment validity. Borrowers should ensure that repayment schedules comfortably fit within the duration of their work pass and income stream. Through ROSHI’s licensed lender network, foreign applicants can access regulated options that emphasise transparent terms and responsible borrowing limits.

Given the applied monthly rates, prudent borrowing remains essential. Loan amounts should correspond directly to documented income and foreseeable employment stability. Singapore’s regulatory framework continues to protect foreign borrowers through defined interest caps, fee limits and mandatory disclosures. By using established platforms such as ROSHI, non‑citizen applicants can evaluate licensed options with greater confidence, balancing urgency, affordability and compliance within a transparent lending environment.

![How to Improving Your Credit Score in Singapore? [Updated Information 2025]](https://stg.roshi.sg/wp-content/themes/roshi/images/new-home-page/expert/e9.png)