Most borrowers pay between 5% to 12% EIR depending on credit score. Advertised rates of 1% to 3% are best case scenarios. Licensed moneylenders charge up to 4% per month.

A medical loan is simply a personal loan used to pay for healthcare related expenses such as hospital bills, surgery, specialist treatments, dental procedures, fertility treatments or medical equipment. Despite marketing names, medical loans are identical to standard personal loans in terms of eligibility, rates and terms. The funds are disbursed directly to the borrower's bank account and can be used for any medical related purpose.

For existing bank customers applying online via Singpass MyInfo, approval can be instant and funds disbursed within minutes to hours. Digital banks like Trust Bank and GXS offer approval in as fast as 60 seconds. Licensed moneylenders can disburse in minutes for urgent medical needs. For planned procedures, apply 1 to 2 weeks in advance to compare options.

Most borrowers pay between 5% to 12% EIR depending on credit score. Advertised rates of 1% to 3% are best case scenarios. Licensed moneylenders charge up to 4% per month.

Borrow up to 4 times monthly income (income below $120k) or 6 to 10 times monthly income (income $120k+). Maximum typically capped at $200,000.

MediSave covers many hospital treatments, surgeries and approved outpatient procedures. Check CPF withdrawal limits before borrowing.

Existing bank customers can get instant approval. Digital banks approve in 60 seconds. Moneylenders disburse in minutes for emergencies.

| What It Covers | Who Qualifies | Key Details | |

|---|---|---|---|

| MediSave | Hospitalisation, day surgery, approved outpatient treatments | All CPF members | Use your own or immediate family members' MediSave. Withdrawal limits apply per procedure. |

| MediShield Life | Large hospital bills, costly outpatient treatments | All SC/PR (compulsory) | Basic coverage with lifetime protection. Premiums payable via MediSave. Covers up to B2/C ward. |

| Integrated Shield Plans | Private hospital, A/B1 ward, higher coverage | Optional top up to MediShield Life | Higher premiums but broader coverage. Riders cover co-payment and deductibles. |

| Medifund | Subsidised bills that remain unaffordable | SC who cannot pay after subsidies | Safety net of last resort. Apply through hospital medical social worker. |

| CHAS | Outpatient care at GP/dental clinics | SC households based on income | Blue/Orange/Green tiers with different subsidy levels. |

| Pioneer/Merdeka Generation | Additional subsidies for seniors | Born 1949 or earlier (PG) / 1950 to 1959 (MG) | Higher MediSave top-ups, outpatient subsidies, MediShield Life premium subsidies. |

| ElderShield / CareShield Life | Severe disability payouts | SC/PR (CareShield Life compulsory from 2020) | Monthly cash payouts if unable to perform daily activities. |

Singapore has one of the most comprehensive healthcare financing systems in the world but many patients don't fully utilise available support. Before taking a loan, check MediSave withdrawal limits for your procedure, file insurance claims through MediShield Life or your Integrated Shield Plan, apply for Medifund if bills remain unaffordable and ask the hospital about interest free instalment plans.

Many patients borrow unnecessarily because they don't realise how much government support is available. A loan should be the last resort not the first response to a medical bill. ![]()

![]()

$1,000

$10,000

1 Months

24 Months

$0.00

$0

$0

| Amount | Public Hospital (Subsidised) | Public Hospital (Private) | Private Hospital |

|---|---|---|---|

| Normal Delivery | $1,500 to $3,000 | $4,000 to $6,000 | $8,000 to $15,000 |

| C-Section Delivery | $3,000 to $5,000 | $7,000 to $10,000 | $15,000 to $25,000 |

| Appendix Removal | $2,000 to $4,000 | $5,000 to $8,000 | $10,000 to $18,000 |

| Knee Replacement | $8,000 to $12,000 | $15,000 to $22,000 | $30,000 to $50,000 |

| Heart Bypass | $20,000 to $35,000 | $40,000 to $60,000 | $80,000 to $150,000 |

| Cataract Surgery (per eye) | $1,500 to $2,500 | $3,000 to $4,500 | $5,000 to $8,000 |

| Cancer Treatment (chemo cycle) | $500 to $2,000 | $2,000 to $5,000 | $5,000 to $10,000 |

| IVF Cycle | $8,000 to $12,000 | — | $15,000 to $25,000 |

| Dental Implant (per tooth) | — | — | $3,000 to $6,000 |

| Invisalign / Braces | — | — | $5,000 to $10,000 |

Apply in under 30 seconds using Singpass or our simple multi-step form. It’s quick, secure and hassle-free.

Review tailored loan options instantly. Our customer success team is here to help with any questions or concerns.

Connect with your preferred lender, finalise all paperwork and receive your funds.

Good intermediary for understanding market trends and knowing many offerings laid out for clarity. Professional and timely sync + scheduling to ensure apt offers and appointments are arranged. Recommended

I used ROSHI platform to find the best loan offers. Just need to fill up some details and wait for loan offers and can choose which one you like. It is totally free and can receive vouchers and cashback based on the loan amount approved. Thank you ROSHI

I used Roshi , to be referred to a trusted lender and got my loan approved.. Would highly recommend anyone to use Roshi for their financial need s. 2 thumbs up.

I am truly grateful to Rosh for helping me find such a professional and reliable lending company. They don’t just provide financial support, but also take the time to understand and guide you with genuine care. Rosh’s assistance made the entire process smooth and reassuring, and I sincerely appreciate the professionalism and dedication.

This guide offers an in-depth look at securing personal loans in Singapore for those with poor credit.

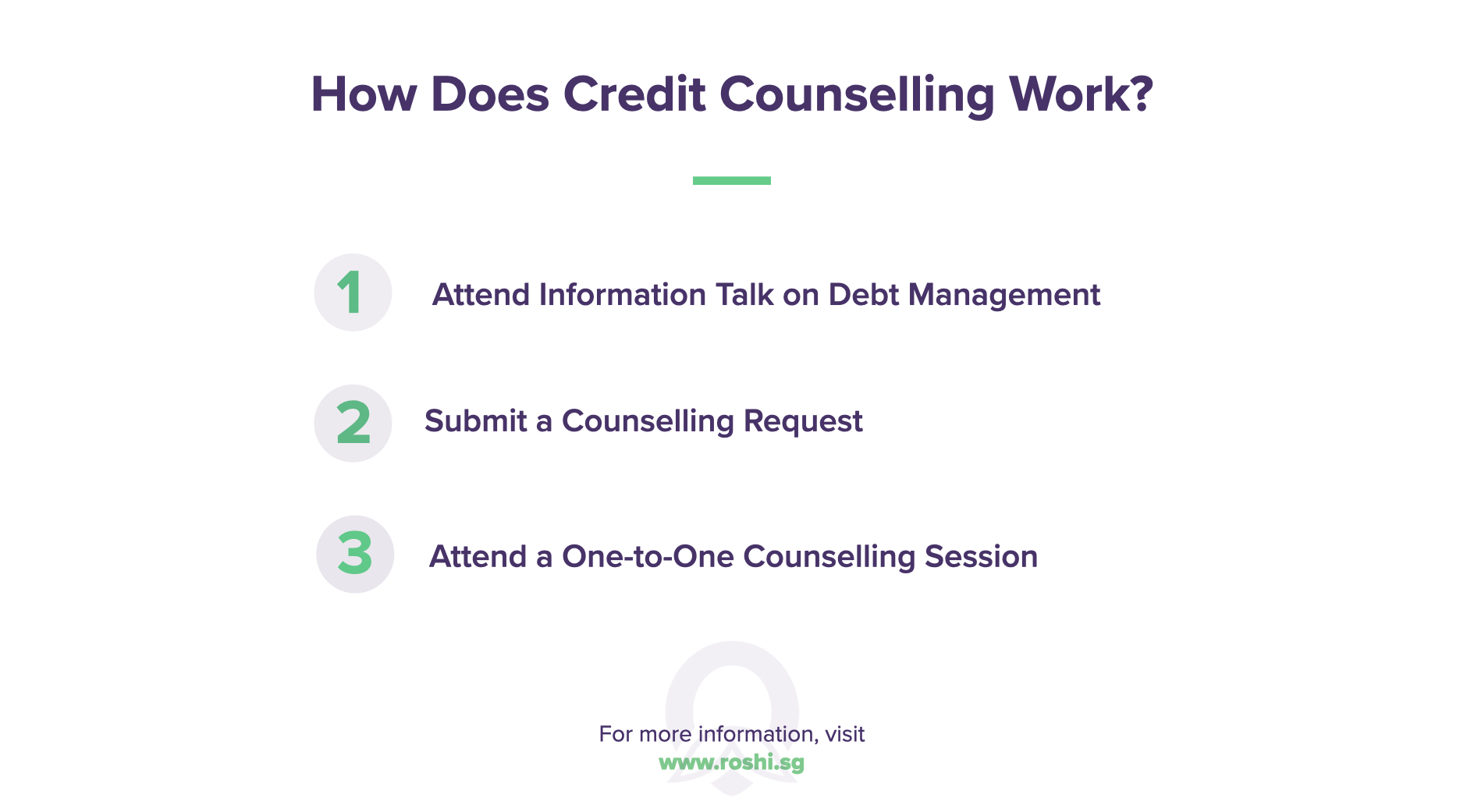

Many people in Singapore need to learn that credit counselling is a solution to helping them organise their finances.

![How to Improving Your Credit Score in Singapore? [Updated Information 2026]](https://stg.roshi.sg/wp-content/themes/roshi/images/new-home-page/expert/e9.png)

Your credit score plays an essential role in your financial health

In the past, the thought of borrowing money was associated with stress

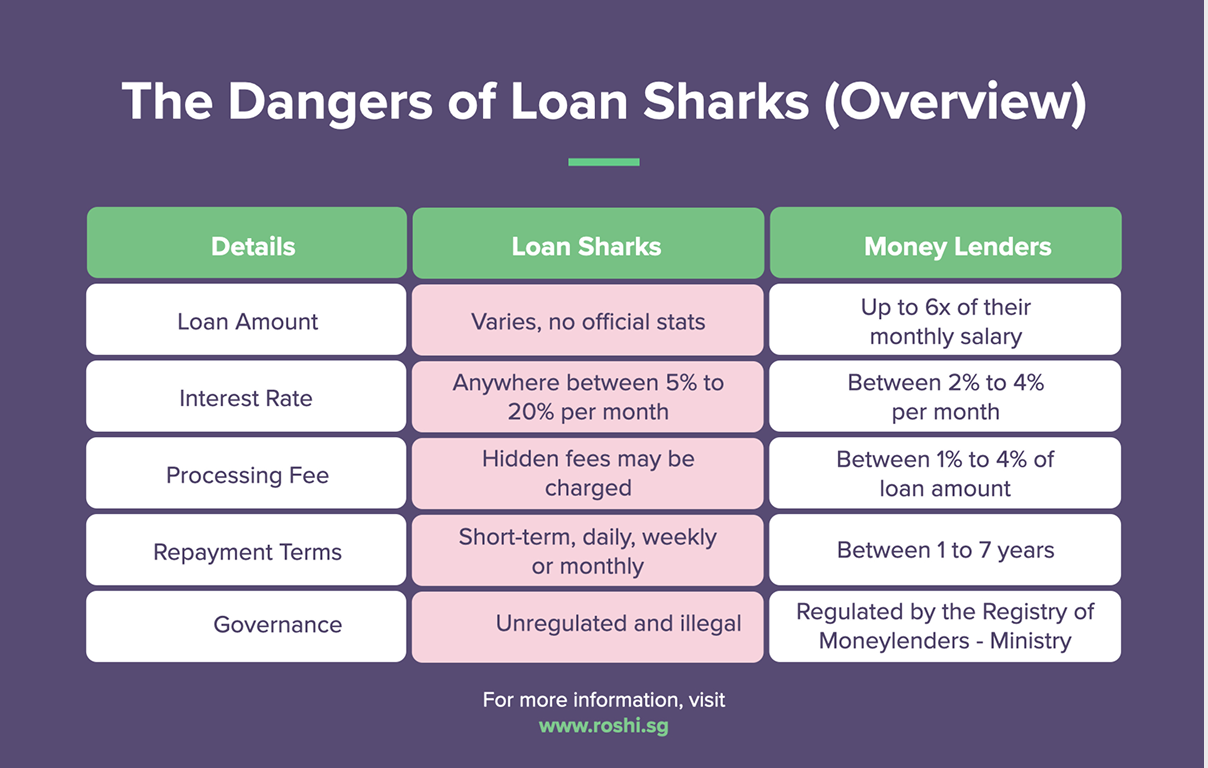

Unanticipated emergencies can push individuals towards loan sharks

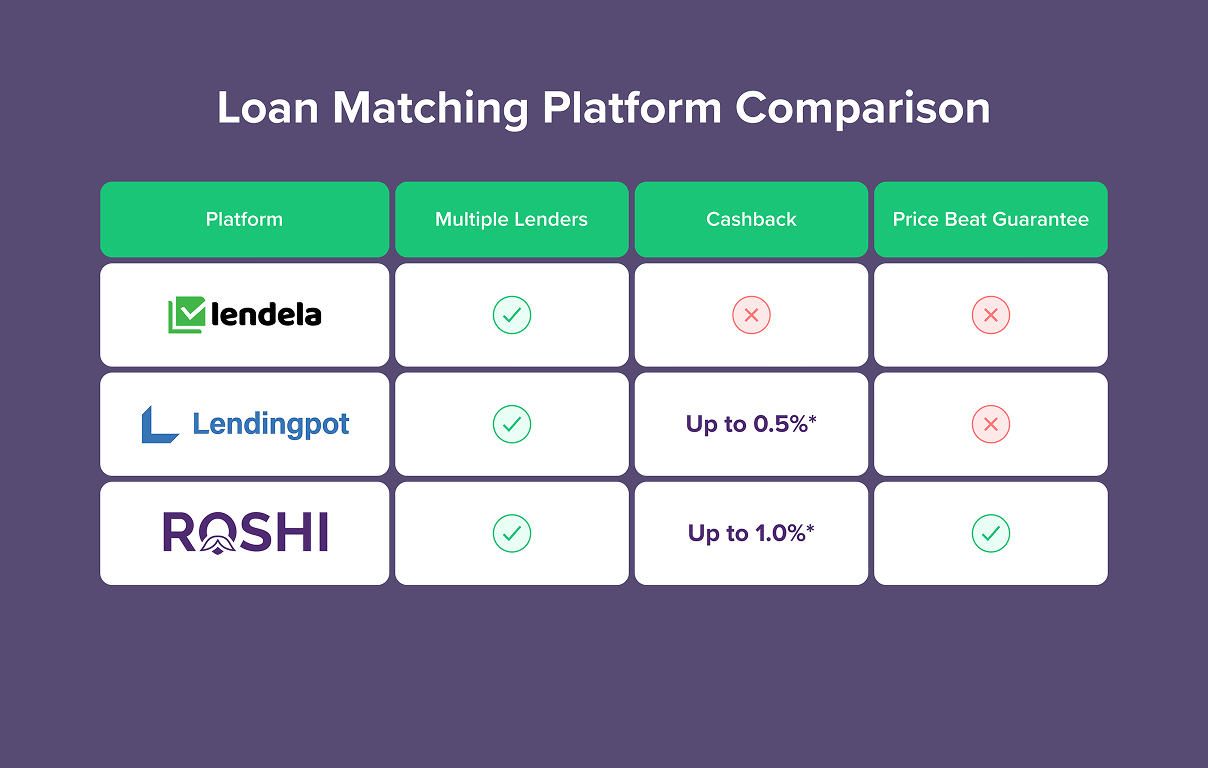

Benefits of Using Personalised Loan Application Platforms.

A medical loan is simply a personal loan used for healthcare expenses but depending on your situation other financing options may be relevant. For general borrowing needs, personal loans from banks and digital lenders offer flexible use funds with competitive rates.

Borrowers needing smaller amounts quickly can explore fast cash loans or emergency loans usually provided by moneylenders.

To estimate monthly repayments and compare options before applying, our personal loan calculator helps model different loan amounts, interest rates and tenures.