Home equity loans are charged at mortgage rates of 2.5% to 4% p.a. which is significantly lower than personal loans from 5% to 14% EIR or credit cards of 26% to 28%.

A home equity loan allows private property owners to borrow against the equity built up in their property which is the difference between the property's current market value and the outstanding mortgage. Also known as cash out refinancing, term loan or mortgage equity withdrawal (MWL) this secured loan provides access to large sums at mortgage level interest rates significantly lower than personal loans.

Home equity loans are available only for private properties such as condominiums, apartments, landed houses and commercial properties and are not available for HDB flats. The loan is subject to MAS regulations including the Loan-to-Value (LTV) limit of 75% and the Total Debt Servicing Ratio (TDSR) of 55%. This page explains how home equity loans work, eligibility requirements, how much can be borrowed and compares options across major banks in Singapore.

A home equity loan lets you borrow money against the value you own in your property. As you pay down your mortgage and your property appreciates, equity builds up this equity can be "cashed out" without selling the property. The loan is secured against your property which means interest rates are similar to home loan rates 2.5% to 4% p.a. rather than personal loan rates of 5% to 14% EIR. Also known as cash-out refinancing, term loan, or mortgage equity withdrawal.

Home equity loans are charged at mortgage rates of 2.5% to 4% p.a. which is significantly lower than personal loans from 5% to 14% EIR or credit cards of 26% to 28%.

Borrow up to 75% of property value minus outstanding loan and CPF used. Potentially hundreds of thousands or millions depending on property value.

Your property secures the loan but failure to repay can result in foreclosure. Only borrow what you can comfortably service.

Repayment tenure up to 35 years or 75 years minus age. Longer tenure = lower monthly payment but higher total interest.

A home equity loan provides access to large sums at low interest rates but your property is on the line. Unlike an unsecured personal loan where the worst outcome is credit damage, failing to repay a home equity loan can result in your home being repossessed and sold by the bank.

Before cashing out equity, ask yourself, can I comfortably service this additional debt if my income drops? Am I using these funds for something that generates returns (investment, business) or something consumable (holiday, car)? The lowest cost loan is still expensive if it puts your home at risk. ![]()

![]()

| Property Value | Outstanding Loan | CPF Used | Equity Available | |

|---|---|---|---|---|

| Purchase | $1,500,000 | $1,125,000 (75% LTV) | $100,000 | $0 |

| Year 5 | $1,700,000 | $1,000,000 | $150,000 | $125,000 |

| Year 10 | $2,000,000 | $800,000 | $200,000 | $500,000 |

| Year 15 | $2,200,000 | $550,000 | $250,000 | $850,000 |

| Fully Paid | $2,500,000 | $0 | $300,000 | $1,575,000 |

| Component | Amount |

|---|---|

| Current property valuation | $2,000,000 |

| 75% of valuation | $1,500,000 |

| Outstanding mortgage | $600,000 |

| CPF used (principal + accrued interest) | $250,000 |

| Maximum home equity loan | $650,000 |

| Amount | Notes | |

|---|---|---|

| Legal Fees | $2,500 to $4,000 | Conveyancing for loan documentation |

| Valuation Fee | $300 to $700 | Bank-appointed valuer assesses property |

| Processing Fee | $0 to $500 | Some banks waive this |

| Stamp Duty | Varies | Only if increasing loan amount above existing mortgage |

| Early Repayment Penalty | 1.5% of amount repaid | If repaying within lock-in period |

| Lock-In Period | 2 to 3 years typical | Penalty applies if exiting early |

| Property Status | Maximum LTV |

|---|---|

| First mortgage, no existing property loan | 75% |

| Second mortgage (already have another property loan) | 45% |

| Borrowing without TDSR assessment | 50% |

A home equity loan provides access to large sums at low interest rates but your property is on the line. Unlike an unsecured personal loan where the worst outcome is credit damage, failing to repay a home equity loan can result in your home being repossessed and sold by the bank.

Before cashing out equity, ask yourself, can I comfortably service this additional debt if my income drops? Am I using these funds for something that generates returns (investment, business) or something consumable (holiday, car)? The lowest cost loan is still expensive if it puts your home at risk. ![]()

![]()

Good intermediary for understanding market trends and knowing many offerings laid out for clarity. Professional and timely sync + scheduling to ensure apt offers and appointments are arranged. Recommended

I used ROSHI platform to find the best loan offers. Just need to fill up some details and wait for loan offers and can choose which one you like. It is totally free and can receive vouchers and cashback based on the loan amount approved. Thank you ROSHI

I used Roshi , to be referred to a trusted lender and got my loan approved.. Would highly recommend anyone to use Roshi for their financial need s. 2 thumbs up.

I am truly grateful to Rosh for helping me find such a professional and reliable lending company. They don’t just provide financial support, but also take the time to understand and guide you with genuine care. Rosh’s assistance made the entire process smooth and reassuring, and I sincerely appreciate the professionalism and dedication.

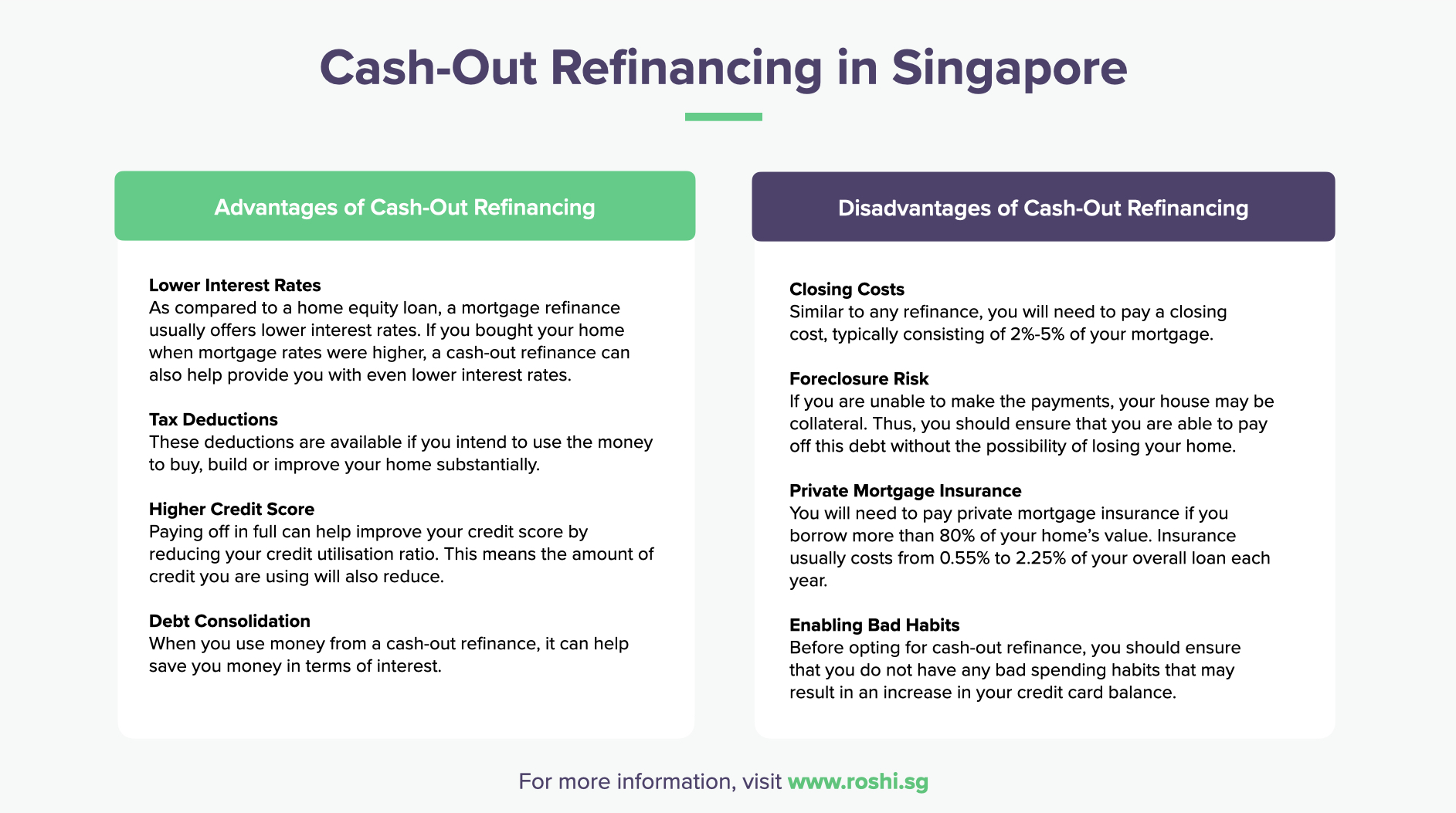

A cash-out refinance is an option that replaces an old mortgage with a new home loan.

Refinancing consists of replacing a current loan with a new one that pays off the debt of the first loan.

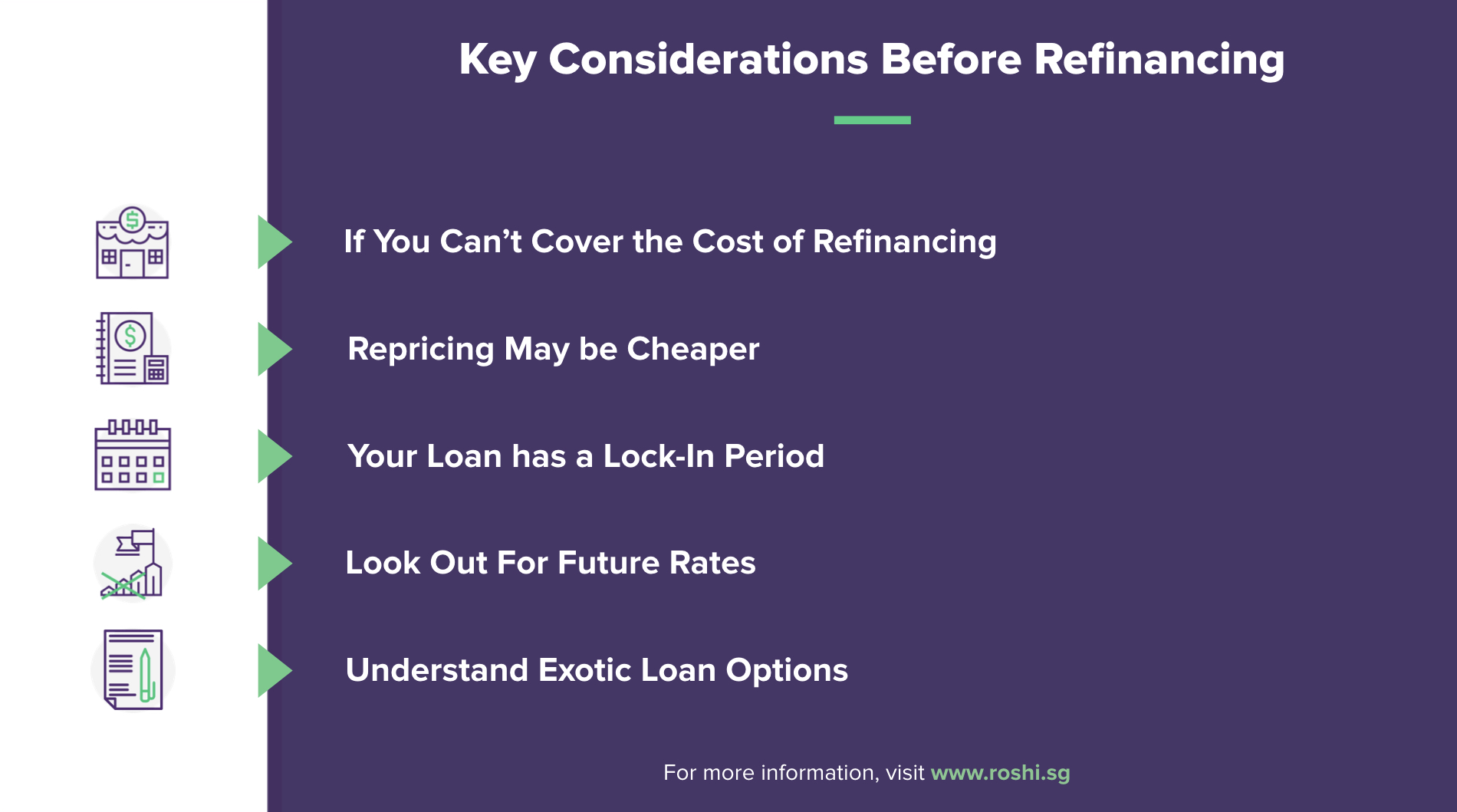

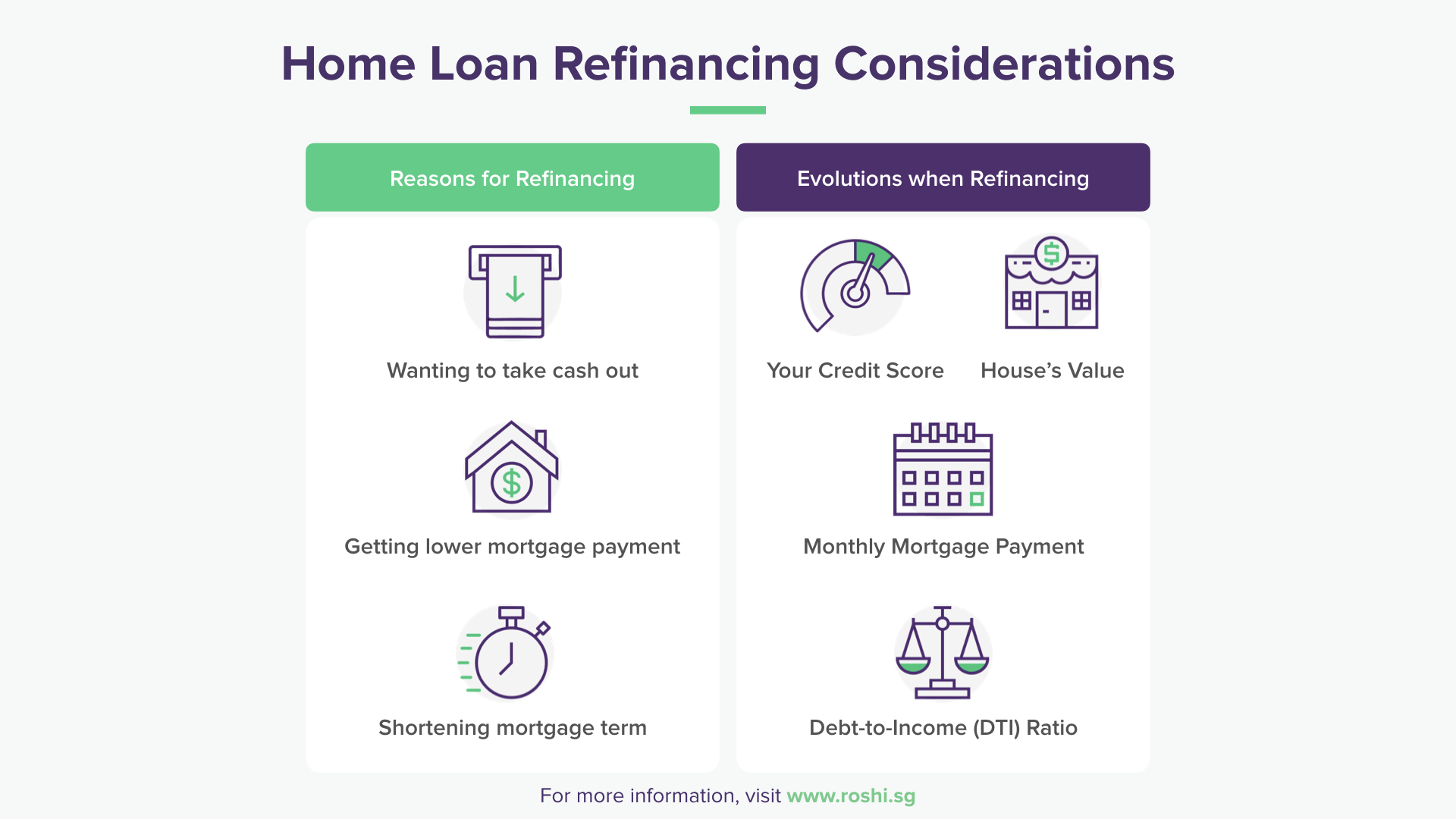

Your decision to refinance your home loan can be due to certain common reasons such as taking cash out, getting a lower payment, or to shorten your mortgage term.

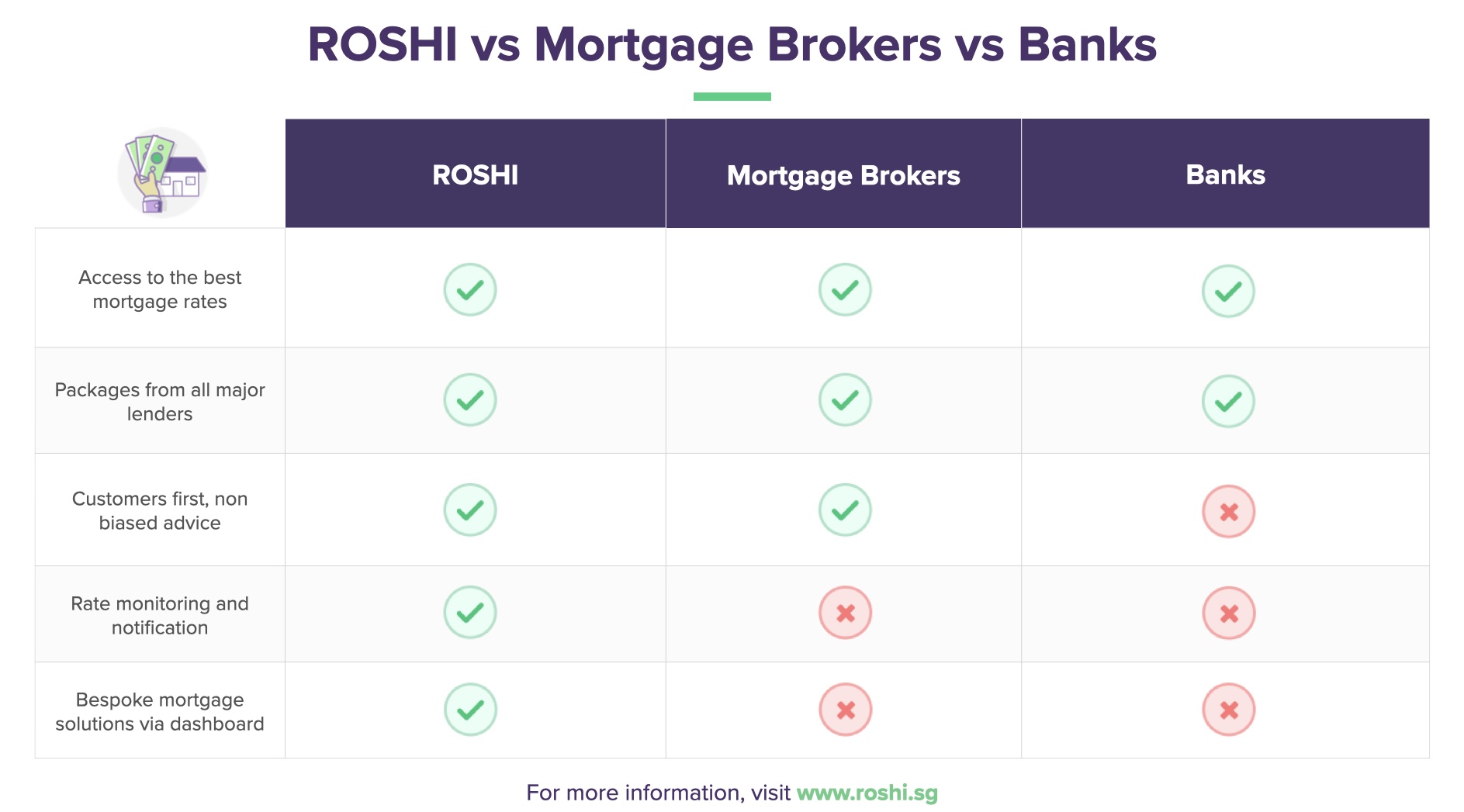

Everyone knows you can go to the bank to get a home loan. If you approached a bank to inquire about home loans, you would be directed to speak with a mortgage staff who is obliged to promote the loans offered by that particular bank. For example, a DBS mortgage staff will only recommend packages offered by DBS.

A home equity loan unlocks the value in your existing property but depending on your situation, other home financing options may be relevant. For investors purchasing a new property, comparing home loans across 15+ banks helps secure the most competitive rates.

Property owners approaching lock-in end can explore refinancing to reduce monthly repayments or switch to a better rate structure.

Our mortgage calculator estimates monthly repayments for different loan amounts and tenures. Our refinance calculator shows potential savings from switching lenders.

For bank specific home loan packages and features, reviews are available for local banks from DBS, OCBC, UOB, Maybank and foreign banks such as HSBC, Standard Chartered, Citibank, CIMB, Bank of China.