Alternative lenders approve in 1 to 3 days while licensed moneylenders approve on the same day. Speed is the core value proposition of bridging loans.

A business bridging loan is short-term financing designed to "bridge" a temporary cash flow gap while your business awaits incoming funds whether from receivables, contract payments, government payouts or funding rounds. Unlike traditional bank business loans that sometimes take days to approve, bridging loans are built for speed with approval as fast as the same day from licensed moneylenders or 3 to 7 days from alternative lenders and banks. Tenures are typically 3 to 12 months with higher interest rates of 1% to 4% per month reflecting the urgency, flexibility and short-term nature of the facility.

Bridging loans are offered by licensed moneylenders, alternative lenders and some banks in Singapore. This page explains when business bridging loans make sense, compares lenders and helps determine whether bridge financing is the right solution for your situation.

A business bridging loan provides fast, short-term capital to cover temporary cash flow gaps until expected funds arrive. It "bridges" the timing mismatch between when you need to pay expenses such as payroll, suppliers or rent and when you'll receive income from customer payments, contract milestones or investment funding. The loan is repaid once the expected funds arrive typically within 3 to 12 months.

Alternative lenders approve in 1 to 3 days while licensed moneylenders approve on the same day. Speed is the core value proposition of bridging loans.

Typically 3 to 12 months. Designed to be repaid when expected funds arrive, not for long-term financing needs.

Alternative lenders charge 0.8% to 2% per month while licensed moneylenders charge 1% to 4% per month. Higher than term loans, but the short tenure limits total cost.

Less stringent requirements than banks. Focus on expected incoming funds and exit strategy rather than lengthy financial history.

The defining question for any bridging loan is: "What funds are coming and when?" A bridging loan only makes sense when you have high confidence in specific incoming funds, a signed contract with milestone payment, confirmed receivables from creditworthy customers or a funding round at term sheet stage. If the expected funds are speculative or uncertain, a bridging loan doesn't solve your problem, it might add expensive debt to an already risky situation.

The higher interest rate is acceptable because the tenure is short but if you're wrong about the timing or the funds don't arrive, that short-term loan becomes a long-term burden at punishing rates. So my advice, know your exit before you sign up for a bridging loan. ![]()

![]()

All lenders verified against Ministry of Law registry. Last updated: July 28 2026.

| Factor | Banks & Alternative Lenders | Licensed Moneylenders |

|---|---|---|

| Loan amount | $100,000 | $100,000 |

| Interest rate | 1.2% per month | 3% per month |

| Tenure | 4 months | 4 months |

| Total interest | $4,800 (1.2% x $100,000 x 4) | $12,000 (3% x $100,000 x 4) |

| Processing fee | $500 | $1,000 |

| Total cost | $5,300 (5.3% of loan amount) | $13,000 (13% of loan amount) |

The total cost difference between providers is significant. A 4-month $100,000 loan costs $13,000 from a moneylender versus $5,300 from a bank or alternative lender. If you have 1 to 3 days rather than 24 hours, the bank or alternative lender saves $7,700.

The question is not just how much the loan costs, but the cost of not having the funds. If missing payroll damages your business reputation or losing a contract costs $500,000 in revenue, a $13,000 bridging cost may be worthwhile.

| Factor | Bridging Loan | Working Capital Loan | Invoice Financing | Business Line of Credit |

|---|---|---|---|---|

| Speed | 24 hours to 1 week | 1 to 3 weeks | 1 to 3 days | 1 to 2 weeks (setup) |

| Tenure | 3 to 12 months | 1 to 5 years | Tied to invoice terms | Revolving |

| Interest Rate | 1% to 4% per month | 7% to 11% p.a. | 1% to 3% per invoice | 8% to 12% p.a. |

| Best For | Urgent, short-term gap | Ongoing operations | Receivables bottleneck | Flexible ongoing needs |

| Exit Strategy | Specific expected funds | General cash flow | Customer payment | Ongoing business |

| Situation | Why It Works |

|---|---|

| Confirmed receivables | Large invoice from a creditworthy customer, payment expected in 30 to 90 days. Clear, predictable exit. |

| Contract awarded, awaiting payment | Government or corporate contract signed, mobilisation payment or milestone payout confirmed. |

| Funding round closing | Investment at term sheet or final due diligence stage, need bridge capital to close. |

| Seasonal inventory purchase | Time-sensitive stock purchase for a known peak season, revenue will cover the loan within months. |

| Project working capital | New project won, need funds for execution, payment terms built into the contract. |

| Short-term cash flow mismatch | Temporary gap between payables and receivables, with clear visibility on resolution. |

| Situation | Why It's Risky |

|---|---|

| Speculative receivables | Customer has not confirmed payment, hoping they will pay, with no guaranteed exit. |

| Early-stage funding discussions | Investment talks are at an exploratory stage with no term sheet, making the timeline uncertain. |

| Chronic cash flow problems | Ongoing operating losses mean a bridge loan only delays the inevitable. |

| Covering accumulated losses | The business is unprofitable and uses bridging finance to stay afloat without fixing the underlying issues. |

| No clear exit strategy | "Something will come up" is not an exit strategy. |

Good intermediary for understanding market trends and knowing many offerings laid out for clarity. Professional and timely sync + scheduling to ensure apt offers and appointments are arranged. Recommended

I used ROSHI platform to find the best loan offers. Just need to fill up some details and wait for loan offers and can choose which one you like. It is totally free and can receive vouchers and cashback based on the loan amount approved. Thank you ROSHI

I used Roshi , to be referred to a trusted lender and got my loan approved.. Would highly recommend anyone to use Roshi for their financial need s. 2 thumbs up.

I am truly grateful to Rosh for helping me find such a professional and reliable lending company. They don’t just provide financial support, but also take the time to understand and guide you with genuine care. Rosh’s assistance made the entire process smooth and reassuring, and I sincerely appreciate the professionalism and dedication.

While credit card promotions can be very attractive, knowing how to manage credit card bills is crucial. Singapore banks like DBS, UOB, and OCBC offer various payment methods for quick payments. Use options across major Singapore banks, from online banking in the comfort of your home to physical AXS machines or simply setting up auto deductions through GIRO.

Starting a business in Singapore? Securing the right startup loan can be the spark that turns your concept into a sustainable company.

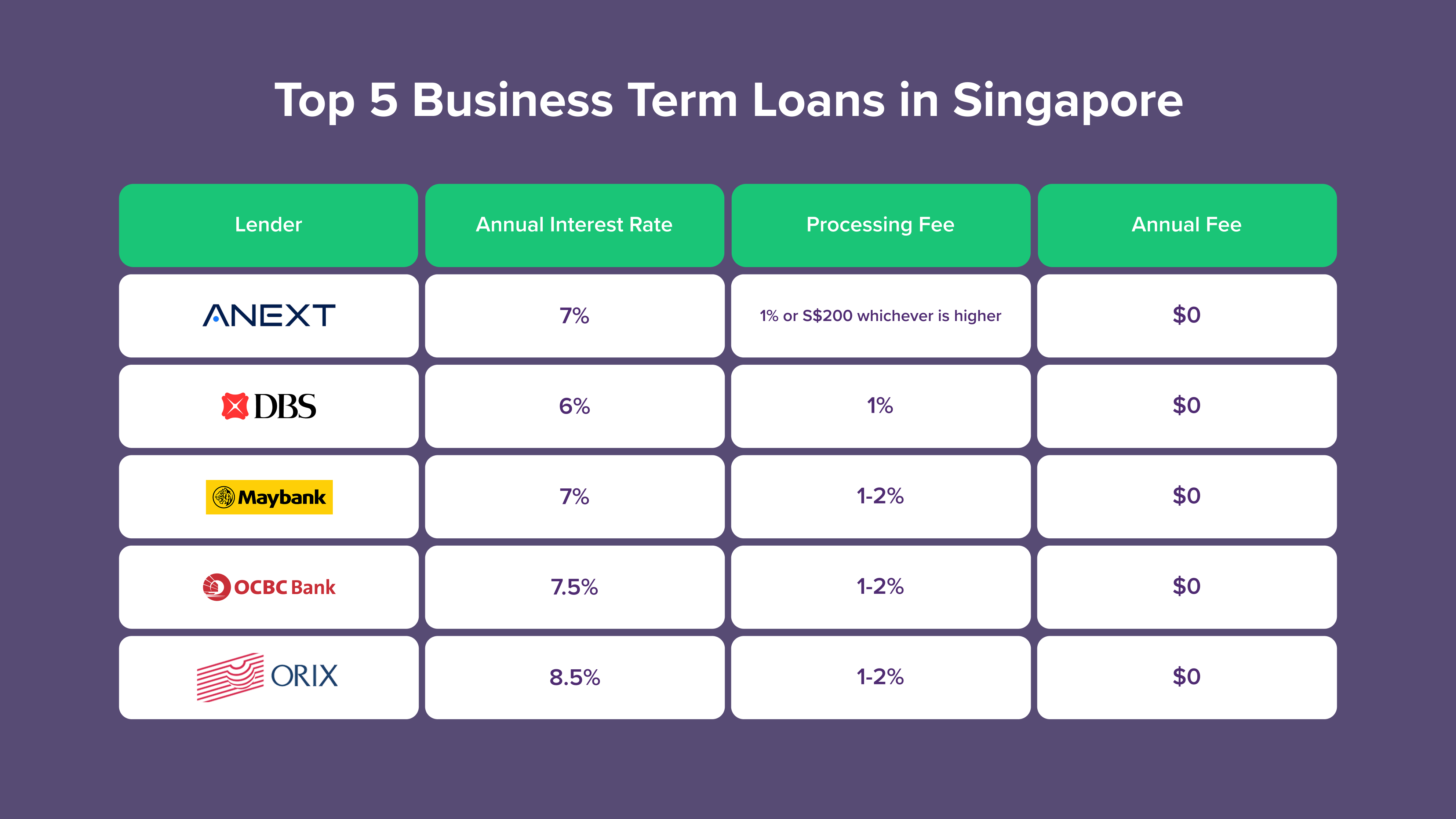

Business term loans in Singapore present a stable financing option with predictable monthly payments and competitive interest rates.

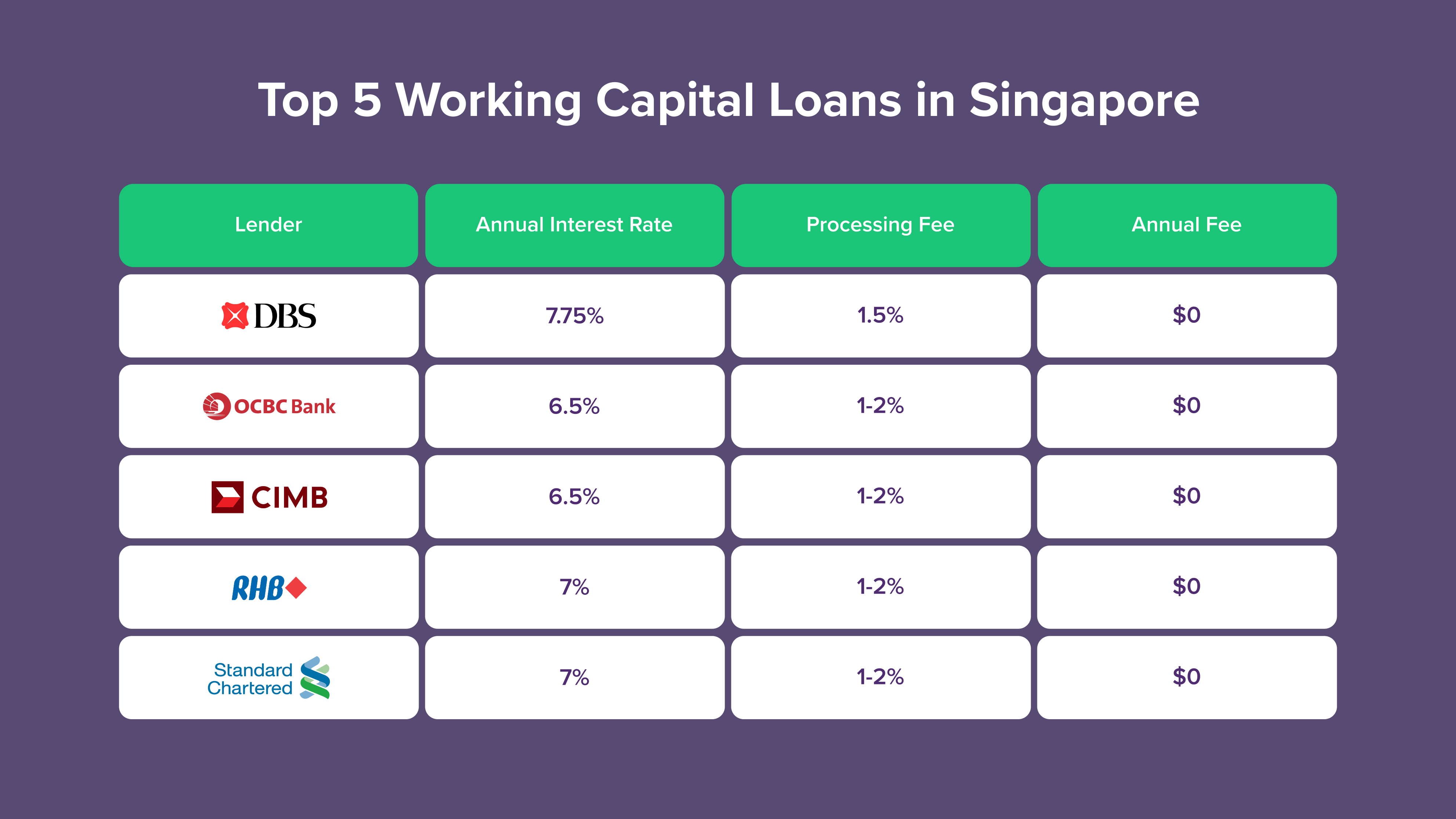

Need extra capital to manage your daily business operations? Working capital loans from Singapore’s leading banks provide a structured and low‑risk solution designed specifically for small and medium‑sized enterprises (SMEs).

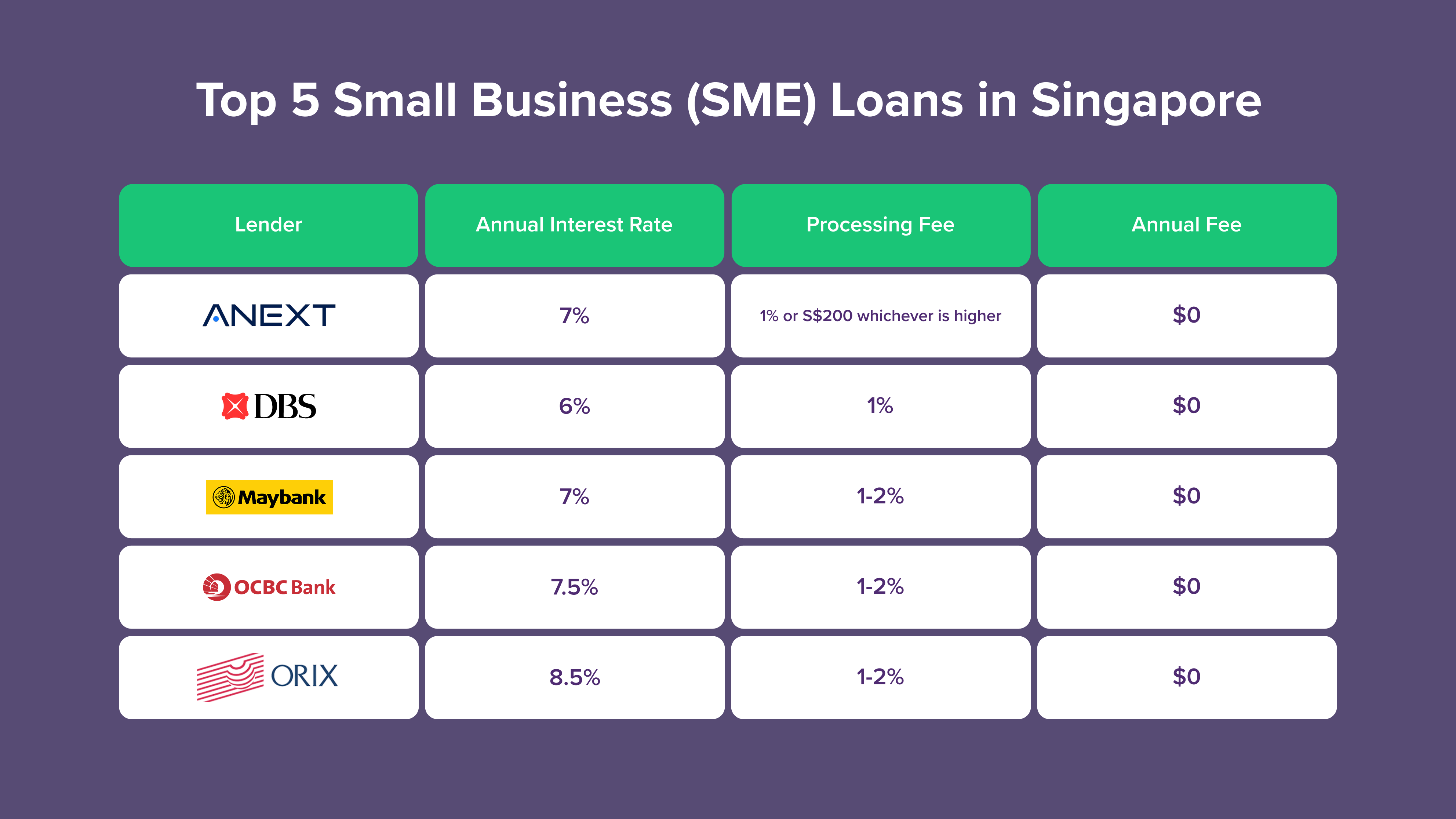

Business bridging loans solve urgent short-term financial gaps, but depending on your situation, other financing options may be more cost effective. For general operational cash flow with more time to apply, working capital loans offer EFS-WCL government support up to $500,000 at lower rates. Small business loans provide lump-sum term financing for expansion or larger projects.

Businesses waiting on customer payments can use invoice financing to convert receivables to cash without term debt, often faster and cheaper than bridging loans for receivables-specific gaps. For ongoing flexible access to funds, a business line of credit provides revolving credit without repeated applications.

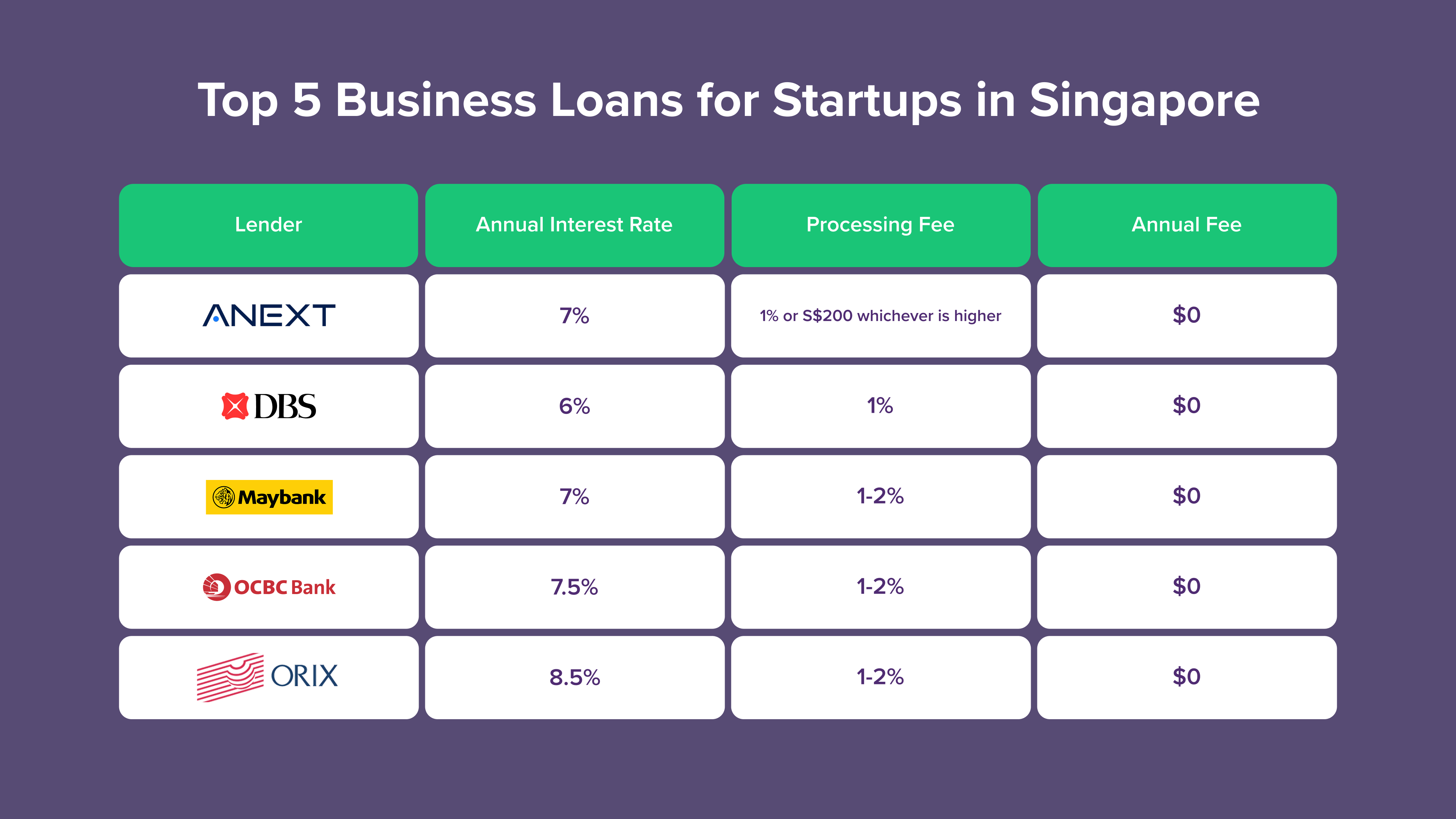

Newer businesses with limited operating history can check business loans for startups with accessible eligibility requirements. Bank-specific bridging loan reviews are available for ORIX, Ethoz, DBS, OCBC, Standard Chartered, Maybank and CIMB.