Unsecured SME loans typically cost 7% to 10% EIR. Government backed schemes and secured loans offer lower rates. Digital lenders charge 9% to 15% for faster approval.

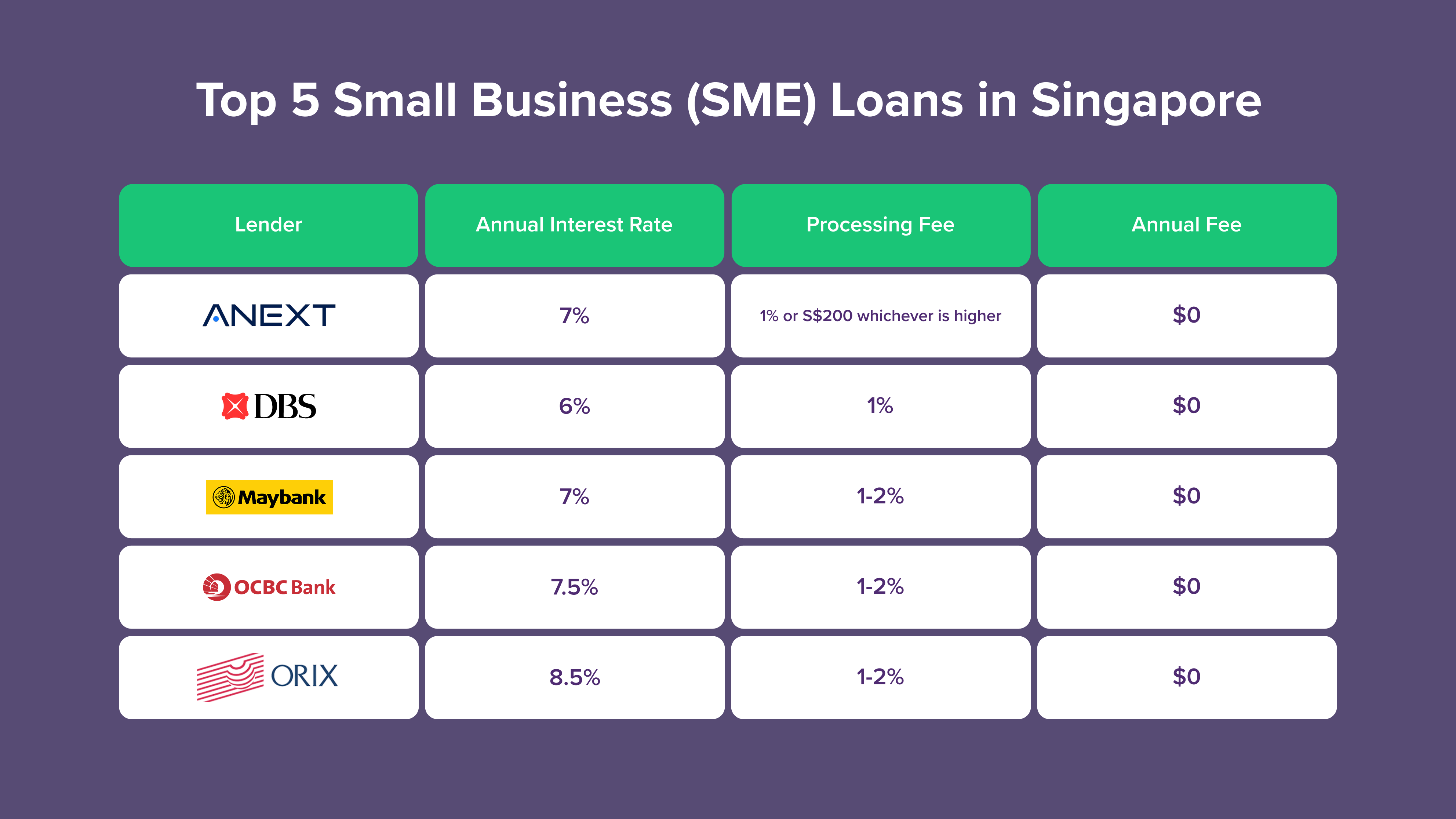

Small business loans also referred to as SME loans provide working capital, equipment financing and growth funding for SMEs registered in Singapore. These loans are offered by banks, alternative lenders and through government backed schemes administered by Enterprise Singapore. Most SME loans are unsecured meaning no collateral is required with loan amounts typically ranging from $50,000 to $500,000 depending on the business's revenue, operating history and creditworthiness.

This page explains the different types of business financing available, eligibility requirements, government support schemes like the Enterprise Financing Scheme (EFS) and how to compare options to find the most suitable loan for your business needs.

A small business loan is financing provided to SMEs (small and medium enterprises) for operational needs, expansion, equipment purchase or cash flow management. Unlike personal loans taken by individuals, business loans are taken by companies, sole proprietorships, partnerships, LLPs or private limited companies registered with ACRA. The loan is assessed based on the company's financial health not just the owner's personal income.

Unsecured SME loans typically cost 7% to 10% EIR. Government backed schemes and secured loans offer lower rates. Digital lenders charge 9% to 15% for faster approval.

Borrow $50,000 to $500,000 unsecured. Secured loans (equipment, property) can reach $30 million. Amount depends on revenue, profitability, and existing debt.

Choose 1 to 5 years for most term loans. Equipment financing up to 7 years. Property loans up to 15 years. Shorter tenure = lower total interest.

Digital lenders approve in 24 to 72 hours. Banks take 3 to 14 days. Government schemes average 3 to 7 days. Complex secured loans take 2 to 3 weeks.

Banks assess risk based on your company's financial health, not just your current situation. The best time to apply for a small business loan is when your financials are strongest which means consistent revenue, positive cash flow and profitability.

Many SMEs make the mistake of waiting until cash flow is tight which reduces approval chances and increases rates offered. Plan ahead and secure credit facilities before you urgently need them. If you're a startup or have limited operating history, consider government backed schemes or digital lenders with more flexible criteria but expect higher rates to compensate for the perceived risk. ![]()

![]()

All lenders verified against Ministry of Law registry. Last updated: July 28 2026.

| Best For | Typical Amount | Tenure | Key Feature | |

|---|---|---|---|---|

| Business Term Loan | General working capital, expansion | $50,000 to $500,000 | 1 to 5 years | Lump sum, fixed monthly repayments |

| Working Capital Loan | Daily operations, payroll, rent | $50,000 to $500,000 | 1 to 5 years | Government risk-sharing available (EFS-WCL) |

| Trade Financing | Import/export, inventory | Up to $10 million | Revolving | Credit line for trade transactions |

| Invoice Financing | B2B with long payment terms | Up to 80% of invoice value | Short-term | Unlocks cash from unpaid invoices |

| Equipment Financing | Machinery, vehicles, technology | Up to $30 million | 1 to 7 years | Secured against the asset purchased |

| Business Overdraft | Short-term cash flow gaps | Varies | Revolving | Pay interest only on amount used |

| Microloan | Startups, small capital needs | Up to $100,000 | 1 to 3 years | Lower requirements for new businesses |

| Purpose | Max Amount | Tenure | Risk Share | |

|---|---|---|---|---|

WCL EFS - SME Working Capital Loan | Daily operations, cash flow | $500,000 | Up to 5 years | 50% to 70% |

TL EFS - Trade Loan | Import/export, inventory financing | $10 million | Revolving | 70% |

FAL EFS - Fixed Assets Loan | Equipment, machinery, premises | $30 million | Up to 15 years | 50% |

PL EFS - Project Loan | Overseas/domestic projects | $50 million | Up to 15 years | 50% to 70% |

VD EFS - Venture Debt | High-growth startups | $10 million | Up to 5 years | 50% to 70% |

ML EFS - M&A Loan | Mergers & acquisitions | $50 million | Up to 5 years | 50% to 70% |

GL EFS - Green Loan | Sustainability projects | Varies by loan type | Varies | 50% to 70% |

Good intermediary for understanding market trends and knowing many offerings laid out for clarity. Professional and timely sync + scheduling to ensure apt offers and appointments are arranged. Recommended

I used ROSHI platform to find the best loan offers. Just need to fill up some details and wait for loan offers and can choose which one you like. It is totally free and can receive vouchers and cashback based on the loan amount approved. Thank you ROSHI

I used Roshi , to be referred to a trusted lender and got my loan approved.. Would highly recommend anyone to use Roshi for their financial need s. 2 thumbs up.

I am truly grateful to Rosh for helping me find such a professional and reliable lending company. They don’t just provide financial support, but also take the time to understand and guide you with genuine care. Rosh’s assistance made the entire process smooth and reassuring, and I sincerely appreciate the professionalism and dedication.

While credit card promotions can be very attractive, knowing how to manage credit card bills is crucial. Singapore banks like DBS, UOB, and OCBC offer various payment methods for quick payments. Use options across major Singapore banks, from online banking in the comfort of your home to physical AXS machines or simply setting up auto deductions through GIRO.

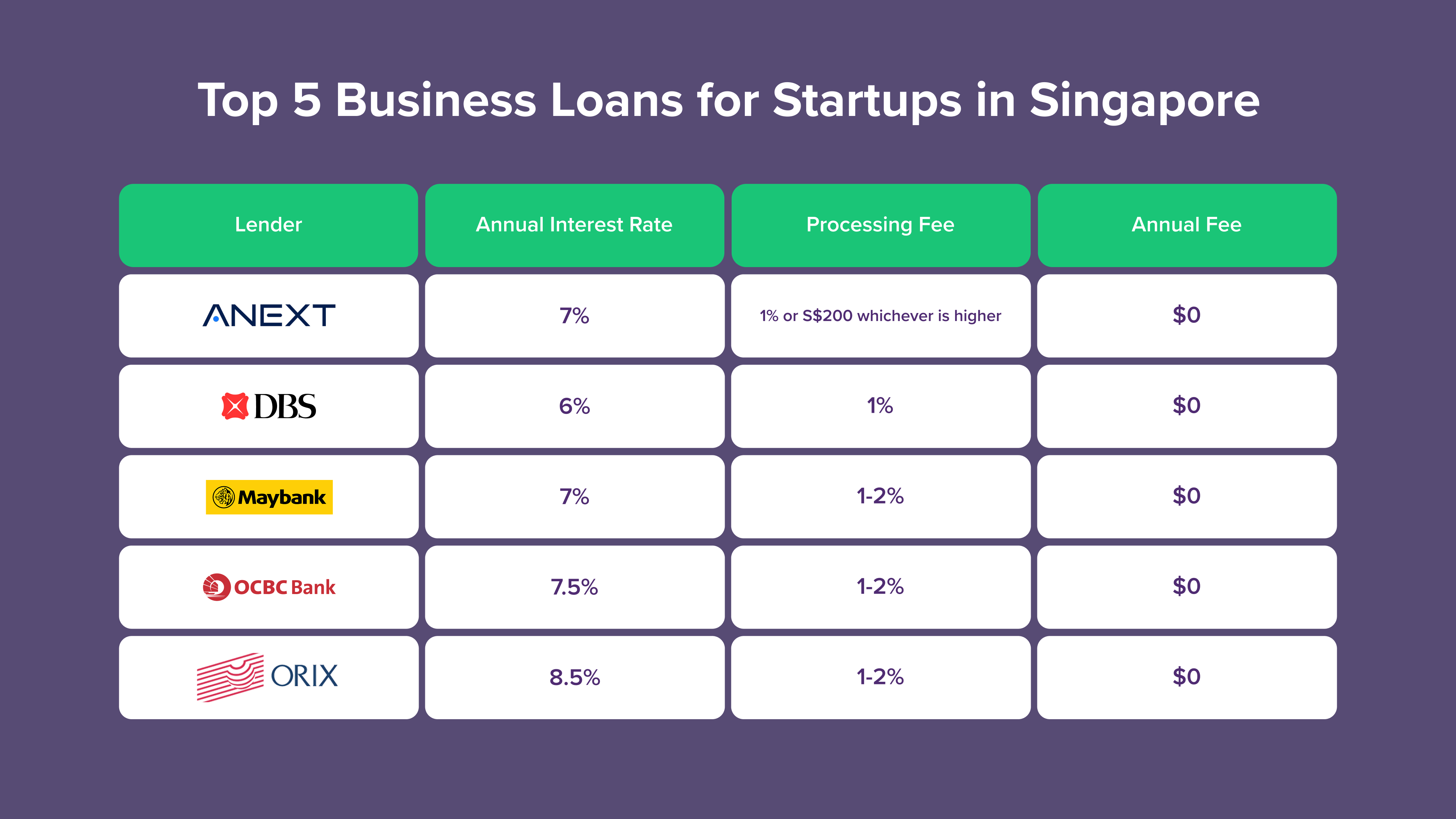

Starting a business in Singapore? Securing the right startup loan can be the spark that turns your concept into a sustainable company.

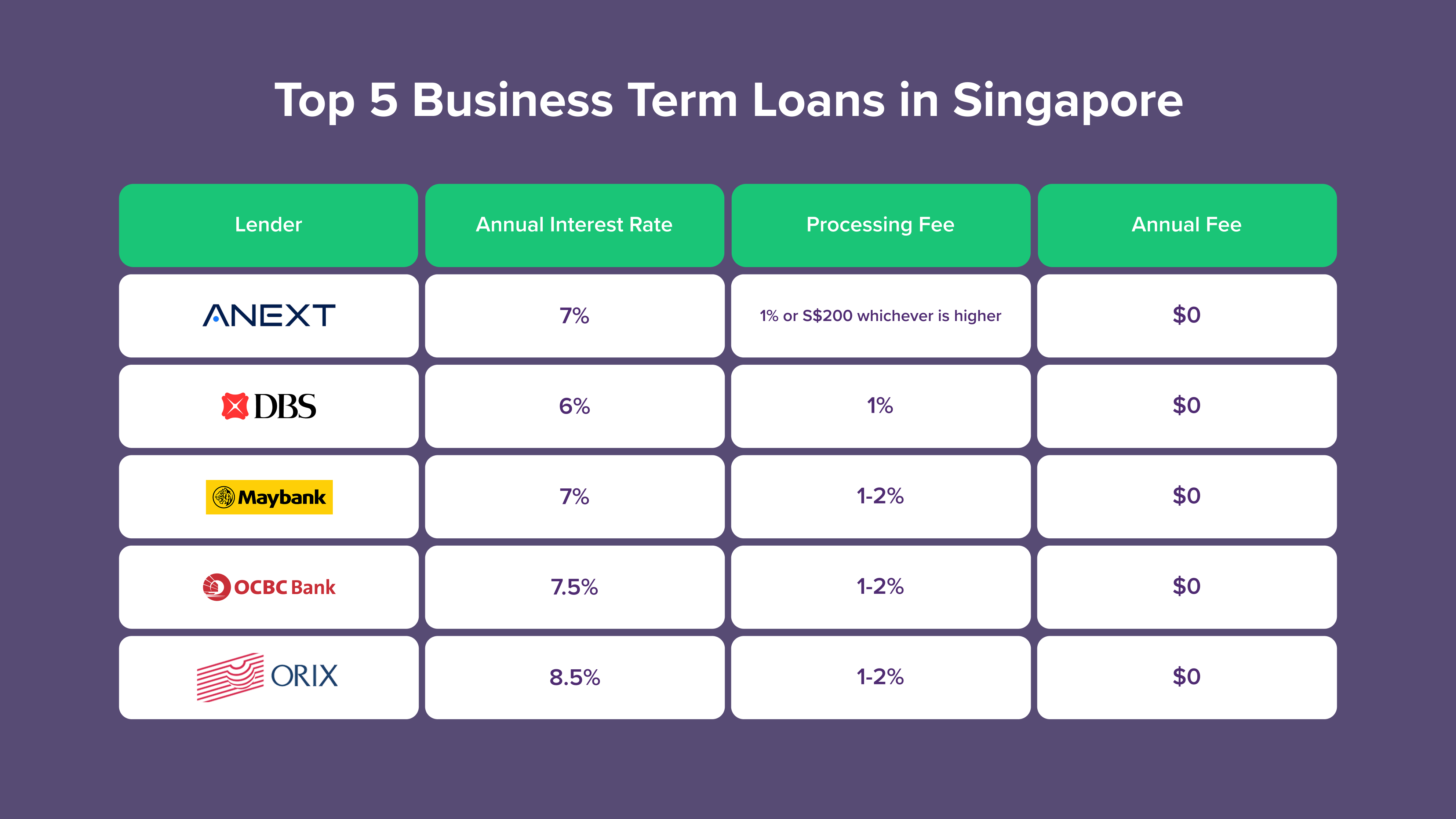

Business term loans in Singapore present a stable financing option with predictable monthly payments and competitive interest rates.

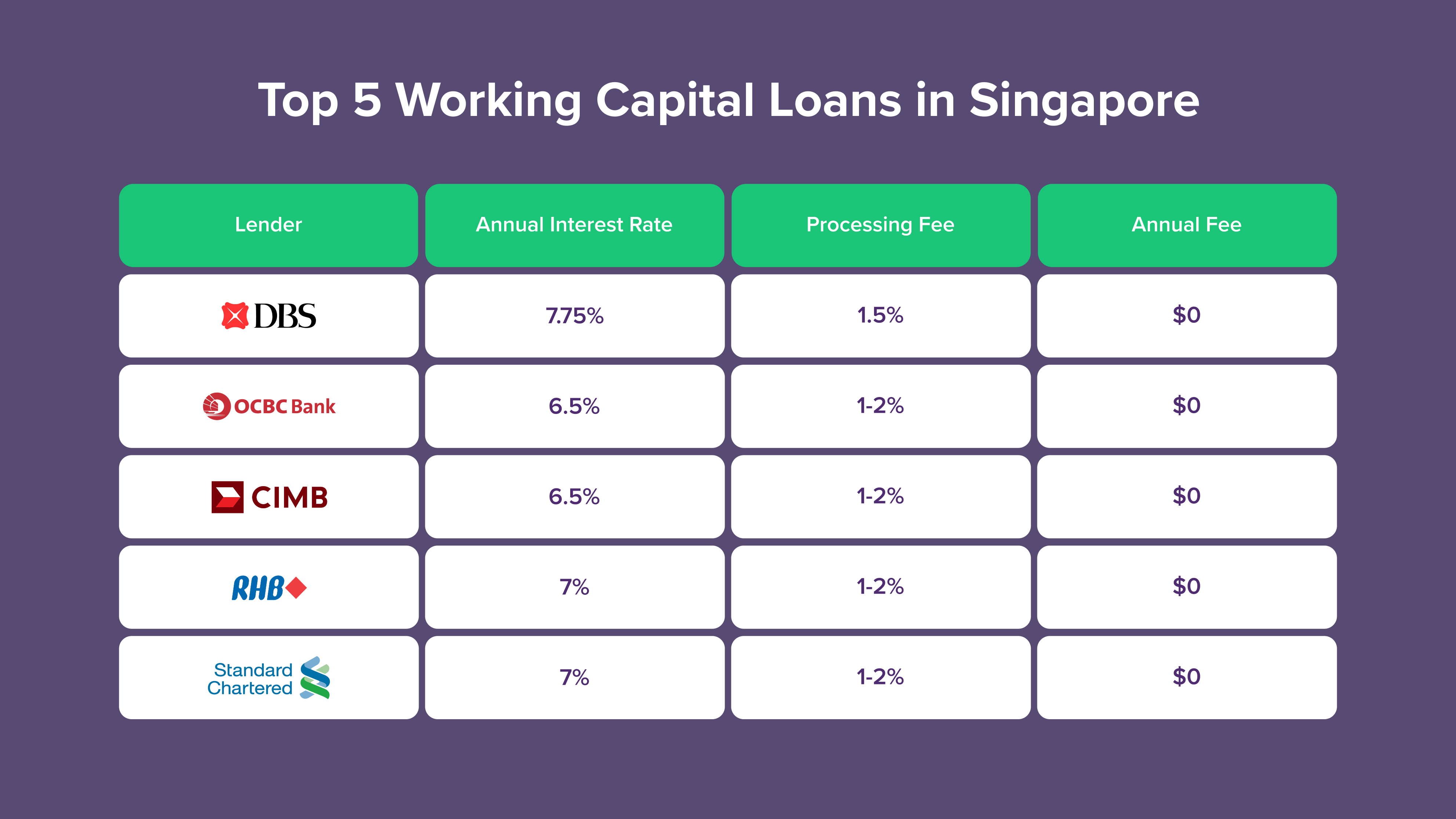

Need extra capital to manage your daily business operations? Working capital loans from Singapore’s leading banks provide a structured and low‑risk solution designed specifically for small and medium‑sized enterprises (SMEs).

Small business loans cover general funding needs but depending on the situation specialised financing options may be more suitable. For short term cash flow gaps working capital loans provide operational funding while bridging loans offer temporary financing between transactions. Startups with limited operating history can explore business loans for startups designed for younger companies and smaller enterprises may qualify for micro business loans with lower thresholds.

For businesses needing to unlock cash tied up in receivables, invoice financing and purchase order financing provide immediate funds without term debt.

For bank specific working capital loan packages reviews are available for DBS, OCBC, UOB, SCB, Maybank, ORIX, Ethoz and Funding Societies.