Being a foreigner doesn't mean you're stuck with bad options

Singapore's moneylending regulations exist to protect borrowers. Interest rates are capped, fees are transparent and every licensed lender must follow the same rules.

The most important thing is to borrow only what you can repay within the agreed repayment timeline. Get your CBS and MLCB reports before applying, have your documents ready and if possible apply early in the month to avoid quota limits. ![]()

![]()

Tips for Foreign Borrowers

How to Improve Your Approval Chances

Your MLCB report shows any outstanding moneylender loans. If you currently have any outstanding loans with other moneylenders, clear those first or make sure your repayment history is clean. Lenders check this before approving your application.

Build local credit history

If you plan to stay in Singapore long-term, get a credit card from a local bank and use it for everyday expenses like groceries and utilities. Pay the full balance monthly. This builds your CBS score over time, which opens the door to bank loans.

Bring a local guarantor

Having a Singaporean or PR act as your guarantor can improve approval chances and may help you secure a lower interest rate. The guarantor must be willing to sign and take on the liability if you default.

Apply early in the month

Licensed moneylenders can only approve 15 foreign borrowers per month. If you apply towards the end of the month, your preferred lender may have already hit their quota.

Only request what you need

Asking for the maximum either $3,000 or $5,000 when you only need $1,500 can reduce your approval chances. Lenders assess whether you can realistically make the repayments so a smaller amount is easier approved.

Ensure your work pass has at least 3 months validity remaining

Lenders need confidence you'll still be employed in Singapore during the repayment period. A pass expiring soon can raise red flags.

Common Mistakes to Avoid

What Foreign Borrowers Get Wrong Most Often

Many foreign loan applications get rejected or end up costing more than they should because of avoidable mistakes. Here are the most common ones we see and how to avoid them.

Interest Rate Trends

Research updated by Trinh Thanh on 6 July 2026 - Moving into July 2026, Singapore’s consumer lending market continues to remain stable with no major changes to statutory interest rate caps, administrative fee limits or licensed moneylending regulations. Licensed moneylenders continue operating within the same regulated framework helping maintain consistent borrowing conditions for Singapore citizens, permanent residents and foreign borrowers.

Demand from foreign borrowers remains steady, particularly among individuals managing relocation expenses, supporting family members overseas or covering temporary cash flow gaps between salary periods. Borrowing activity continues to focus mainly on practical financial needs rather than discretionary spending. Compared to June, rate trends and approval conditions have remained largely unchanged with lenders continuing to place stronger emphasis on employment stability, valid work passes, income documents and repayment capacity.

As of July 2026, licensed moneylenders regulated by Singapore’s Registry of Moneylenders continue to remain one of the more accessible financing options for foreign borrowers. Average monthly interest rates continue to stay around 3.8%, remaining slightly below the legal cap of 4% per month. These rates continue to reflect Singapore’s regulated lending structure and the additional assessment factors commonly associated with lending to non-citizens.

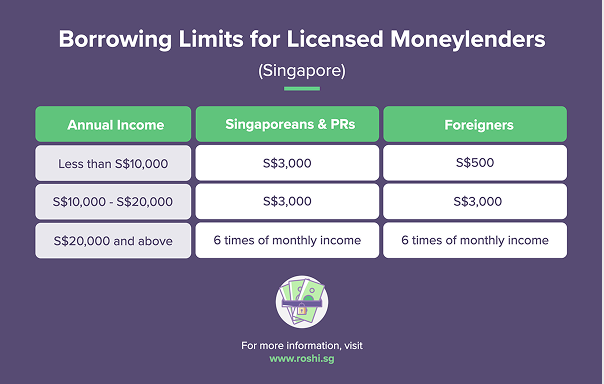

Foreign applicants may still qualify for loan amounts of up to six times their monthly income subject to income level and regulatory borrowing limits. Under Singapore’s licensed moneylending framework, foreigners residing in Singapore may borrow up to six times monthly income when annual income is at least S$20,000. For lower income brackets, smaller limits apply. Foreigners earning below S$10,000 annually may borrow up to S$500 while those earning from S$10,000 to below S$20,000 may borrow up to S$3,000.

The maximum interest rate licensed moneylenders can charge remains 4% per month and permitted fees include an administrative fee of up to 10% of the loan principal and a late repayment fee not exceeding S$60 for each month of late repayment.

In practice, approved amounts continue to depend closely on verified income, employment consistency, work pass duration, MLCB records and overall repayment capacity. Most applications can still be started online allowing borrowers to submit basic details and supporting documents digitally before visiting the lender’s office.

However, Singapore regulations continue to require borrowers to complete identity verification and sign loan agreements in person before funds can be released. Once this process has been completed many licensed moneylenders are still able to finalise approvals and disburse funds within the same working day.

Banks in Singapore continue to provide personal loan products for some foreign applicants, although approval standards remain more selective compared to licensed moneylenders. In most cases, these products continue to target expatriates with stronger credit scores, higher income levels and more stable long term employment arrangements in Singapore.

For approved applicants, bank loans generally continue to offer lower effective interest rates particularly for longer repayment periods. However, the application process remains more detailed and may include CBS statements, income verification, employment contract review and supporting document checks. Approval timelines can also continue to extend across several business days before funds are released.

For many foreign workers, especially those seeking smaller or more urgent financing, these requirements may continue to limit accessibility. As a result, banks may provide lower overall borrowing costs for well-qualified applicants while licensed moneylenders continue to remain the more practical option for faster short term financing.

In July 2026, foreigner loans continue to reflect the balance between accessibility, repayment planning and regulatory structure within Singapore’s consumer lending market. Licensed moneylenders remain one of the more responsive financing channels for foreign borrowers, offering quicker approvals at monthly interest rates close to 3.8% within a regulated environment. Bank financing continues to serve a smaller group of applicants who are able to meet stricter approval requirements.

From ROSHI’s perspective, foreign borrowers should continue paying close attention to how repayment periods align with employment duration, salary cycle and work pass validity. Loan commitments that fit comfortably within the borrower’s income stability and legal stay period are generally easier to manage over time.

Through ROSHI’s platform, borrowers are also able to compare licensed lending options more easily, review loan terms clearly and make decisions based on urgency, affordability and repayment readiness.

For foreign borrowers in July 2026, Singapore’s consumer lending market continues to remain accessible and regulated with different financing options depending on income level, employment status and credit profile. Licensed moneylenders still provide relatively fast access to financing, particularly for borrowers who may not fully meet traditional bank lending requirements. Although in-person verification remains mandatory, the overall process generally continues to remain efficient for most applicants.

Given the monthly interest rates applied to short term borrowing, repayment planning continues to remain important. Borrowers who align loan amounts carefully with income consistency, employment duration and work pass validity are generally better positioned to avoid unnecessary financial pressure.

Within Singapore’s regulated consumer lending environment, borrowers who compare loan terms carefully and align loan commitments with repayment capacity continue to be better positioned to make informed and responsible borrowing decisions.

![How to Improving Your Credit Score in Singapore? [Updated Information 2025]](https://stg.roshi.sg/wp-content/themes/roshi/images/new-home-page/expert/e9.png)